You’re staring at the screen. The tax software just spit out a number, and honestly, it looks like a typo. Maybe it’s lower than last year. Maybe it’s so high you’re already mentally spending it on a weekend trip or finally fixing that rattling sound in your car. But here is the thing: that initial estimate of tax refund you see in February is rarely the check that actually hits your bank account in April. It’s a flickering image. A guess.

The IRS processed over 150 million individual tax returns last year, and a massive chunk of those taxpayers walked away with a refund averaging around $3,000. But "average" is a dangerous word in finance. Your neighbor might be getting five grand back because they had a kid and started a side hustle, while you’re staring at a $200 pittance because your HR department actually did their job correctly for once. Tax season is basically the Olympics of paperwork, and if you don't know how the math works, you're going to be disappointed.

Why that early estimate of tax refund feels like a lie

Most people use a calculator to get a quick vibe of their situation. You plug in your salary, maybe your filing status, and boom—the site gives you a number. It feels official. It isn't.

Those quick calculators usually ignore the "above-the-line" deductions. They forget about that $300 you donated to the local shelter or the student loan interest that’s been eating your soul. More importantly, they often miss the subtle shift in tax brackets. For the 2025 tax year (filing in 2026), the IRS adjusted the brackets for inflation by about 2.8%. If your raise didn't outpace inflation, you might actually find yourself in a lower effective tax bracket, which totally flips your estimate of tax refund on its head.

Think about your W-4. When did you last touch it? Probably when you were hired three years ago and had no idea what "exemptions" meant. If you’ve had a kid, bought a house, or even just gotten married, that old W-4 is sabotaging your refund. Or worse, it’s giving you a huge refund that basically amounts to an interest-free loan you gave the government all year. Why let them hold your money for free?

The phantom "Refund Shock" and the Child Tax Credit

Let's talk about the big one. The Child Tax Credit (CTC) is a monster of a variable. In recent years, we’ve seen legislative tug-of-wars over how much of this credit is "refundable." For 2025, the maximum credit remains $2,000 per qualifying child, but only a portion of that is refundable—meaning if you owe zero taxes, you only get a specific amount back as a check. If you’re banking on a huge windfall based on 2021-era rules, you’re going to be frustrated.

I talked to a CPA in Chicago last week who said her biggest headache is "refund shock." People come in expecting $6,000 because they saw a TikTok about "tax hacks," but they forget they stopped paying into their 401(k) or took a freelance gig that didn't withhold a cent. That 1099-NEC income? It’s a refund killer. It’s like a vacuum for your estimate of tax refund, sucking up the surplus you built through your 9-to-5 job to cover the self-employment tax.

Deductions: Standard vs. Itemized is a high-stakes game

Almost 90% of Americans take the standard deduction. It’s easy. It’s safe. For 2025, it’s $15,000 for singles and $30,000 for married couples filing jointly. But if you’re living in a high-tax state like California or New York, or if you’ve got massive medical bills, you might be leaving money on the table.

- The SALT Cap: You can only deduct up to $10,000 for state and local taxes. If you paid $15,000 in property tax, that extra $5,000 is just... gone. It doesn't help you.

- Medical Expenses: You can only deduct the part that exceeds 7.5% of your Adjusted Gross Income (AGI). If you make $100k, you need over $7,500 in bills before the first penny counts.

- Charity: If you aren't itemizing, those Goodwill receipts are basically bookmarks. They won't change your refund estimate at all.

It’s kind of a bummer. You do all this "good stuff" all year, and the tax code just shrugs because the standard deduction is already so high. To really move the needle on your estimate of tax refund, you have to look at "credits," not just deductions. Credits are dollar-for-dollar. They’re the heavy hitters. The Earned Income Tax Credit (EITC) is the king here, potentially putting over $7,000 back in the pockets of low-to-moderate-income families with three or more kids.

The "Hidden" math: Why your paycheck isn't telling the whole story

Most people think of taxes as a flat percentage. It’s not. It’s a bucket system. Your first $11,600 (for singles) is taxed at 10%. The next chunk at 12%. And so on. When you get a bonus at work, the payroll software often "withholds" as if you make that bonus every single week of the year. It puts you in a fake high bracket. Then, when you file your return, the IRS realizes you aren't actually a millionaire and gives that "over-withheld" money back.

That is literally all a refund is. It’s a correction of an error.

If you want an accurate estimate of tax refund, you need to look at your "Total Tax Liability" from last year's Form 1040 (Line 24). Compare that to your total withholding on your final paystub of the year. If you’ve paid in $12,000 and your tax is $10,000, you get $2,000. It’s simple, but people make it so complicated by focusing on the "refund" instead of the "tax."

Real-world weirdness: Solar panels and EV credits

Energy credits are the wild west right now. If you installed solar panels in 2025, you’re looking at a 30% Residential Clean Energy Credit. That’s massive. If the system cost $20,000, that’s a $6,000 credit. If your tax bill was $5,000, that credit wipes it to zero. But wait—that specific credit isn't refundable. You don't get a $1,000 check for the "extra." You just carry it forward to next year.

This is where the online calculators fail. They see "$6,000 credit" and add it to your estimate of tax refund total, but the IRS rules might just say "cool, you owe nothing, but we aren't paying you the difference." It’s heart-breaking to see a $5,000 refund estimate drop to $0 because of a misunderstanding of "non-refundable" vs "refundable."

How to actually nail down your numbers

Forget the "30-second estimators." They’re marketing tools for tax software. If you want a real estimate of tax refund, you need to do the heavy lifting manually or with a pro.

- Gather the 1099-INTs from your bank. Yes, even that $14 in interest from your savings account counts. The IRS gets a copy, and if you don't report it, they’ll flag your return, delaying your refund by months.

- Check your HSA contributions. If you put money in through payroll, it’s already tax-free. If you put it in yourself, you get a deduction that lowers your AGI.

- Look at your "Qualified Business Income" if you’re a freelancer. The QBI deduction is a 20% haircut on your taxable business income, and it's one of the biggest ways to boost your refund that people totally overlook.

The final reality check

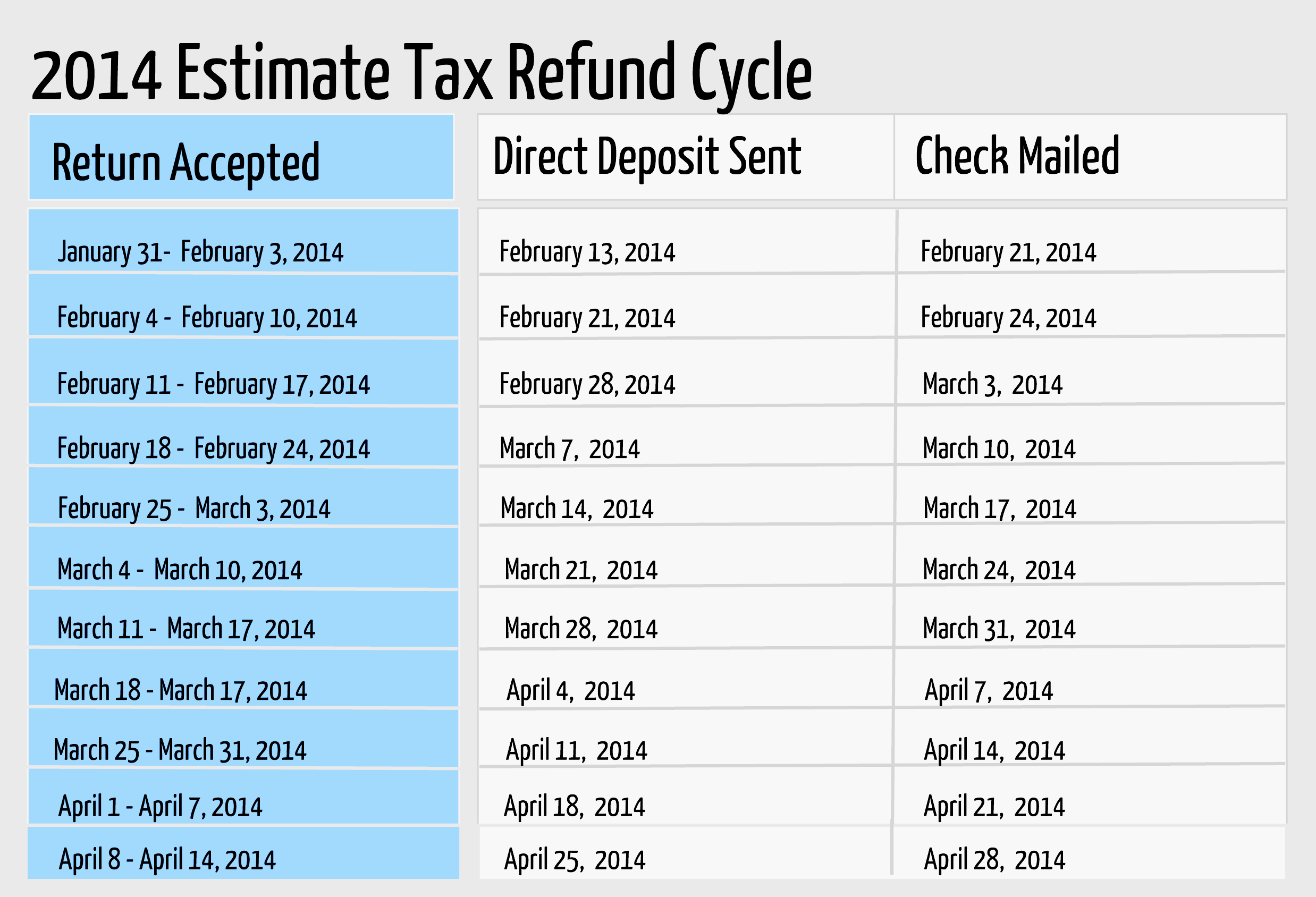

The IRS usually starts accepting returns in late January. If you file electronically and choose direct deposit, you’ll likely see your money in 21 days or less. But if you claim the EITC or the Additional Child Tax Credit, the PATH Act legally forbids the IRS from issuing your refund before mid-February. No matter what your estimate of tax refund says, the calendar is the boss.

Don't panic if your number changes as you finish your return. Adding one more form—like a 1099-DIV for some stocks you sold—can cascade through the whole return. It changes your AGI, which might change your eligibility for certain credits, which shifts the final number. It’s all connected.

Your next moves for a better refund

Instead of just waiting and hoping, take these steps to solidify your financial position before the filing deadline.

- Adjust your W-4 immediately: If your refund is over $3,000, you are overpaying the government every month. Lower your withholding and put that extra $250 a month into a high-yield savings account or your 401(k).

- Max out your IRA by April 15: You can still contribute to a traditional IRA for the previous tax year up until the filing deadline. This is one of the few ways to "lower" your 2025 taxes after the year has already ended. It directly increases your refund.

- Download your "Tax Transcript": Go to the IRS website and get your official transcript. It shows exactly what the IRS has on file for you (W-2s, 1099s). This prevents the "missing form" errors that cause refund delays.

- Verify your bank info twice: A single transposed digit in your routing number will turn a 10-day direct deposit into a 6-week paper check nightmare.

- Use the IRS Free File tool: If your AGI is $79,000 or less, don't pay for software. Use the free tools provided by the IRS to keep more of your money.