Most people treat a bank statement like that annoying piece of mail they'll "get to eventually," or worse, a digital notification that gets cleared without a second thought. It's boring. Honestly, it's just a long list of numbers and weirdly abbreviated merchant names that look like someone fell asleep on a keyboard. But if you're ignoring these documents, you're basically leaving your front door unlocked in a bad neighborhood.

A bank statement is more than just a summary of what you spent at Starbucks or how much you dropped on Amazon last month. It is a legally binding record of your financial life. If there is a mistake—and banks make them more often than you’d think—that PDF is your only shield.

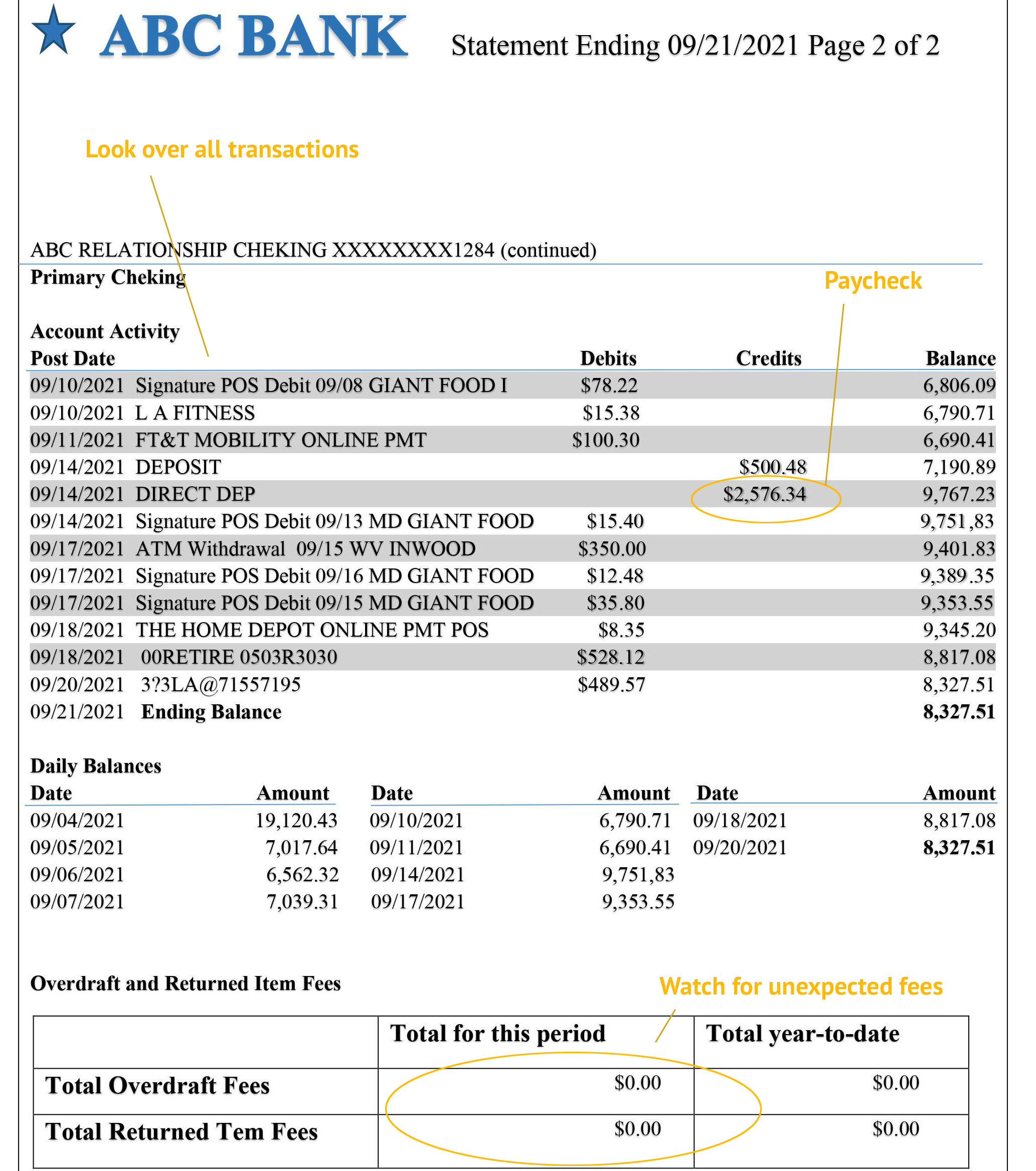

What a Bank Statement Actually Tells You (And What It Doesn’t)

At its core, your bank statement is a formal document issued by your financial institution, typically every month, that summarizes every single transaction within a specific "statement cycle." This cycle doesn't always align with the first and last day of the month. It might run from the 15th to the 14th. You've got to check the header to be sure.

You'll find your starting balance, every deposit, every withdrawal, and that final closing balance. But here is where it gets tricky. People often confuse their "available balance" in their banking app with the balance on their statement. They aren't the same. Your app shows real-time data, including "pending" charges that haven't actually cleared the banking system yet. The statement is the history of what is settled.

Think of it this way: the app is a live stream, but the statement is the high-definition replay.

The Anatomy of the Document

You usually see the bank’s logo at the top left. Right next to it or just below, you’ll see your account number—usually masked for security—and the period the statement covers. If you’re applying for a mortgage or a car loan, lenders look at these dates religiously. They want to see "seasoned funds," which is just a fancy way of saying they want to make sure that $10,000 deposit didn't just appear out of nowhere two days ago.

Then comes the transaction list. This is the meat of the bank statement. You’ll see "ACH" transfers, which are usually your direct deposits or automated bill pays. You’ll see "POS" transactions, which are your point-of-sale debit card swipes. Sometimes you’ll see weird codes like "REVERSAL" or "ADJUSTMENT." If you see those and you didn't call the bank to complain about a fee, pay attention. The bank might be fixing its own mistake, or they might be taking money back.

Why You Must Scan for "Zombie" Subscriptions

We've all done it. You sign up for a free trial of a streaming service or a fitness app, promising yourself you'll cancel it in six days. You don't. Six months later, you're still paying $14.99 a month for something you haven't opened once.

When you sit down with your bank statement, you're looking for these zombies. Small amounts—$5.99 here, $9.00 there—are designed to blend into the background. They rely on the fact that most people just look at the big numbers. If you find a charge you don't recognize, Google the merchant ID. Often, a company's billing name is totally different from their brand name. "LMN* Services" might actually be that yoga app you downloaded on a whim.

The 60-Day Rule You Can't Afford to Ignore

Here is a bit of "inside baseball" from the banking world. Under the Electronic Fund Transfer Act (Regulation E), you generally have a 60-day window from the date your bank statement was sent to you to report errors or unauthorized transactions.

If you wait 61 days? You might be out of luck.

If someone stole your debit card info and has been charging $20 a week for gas, and you don't notice for three months, the bank isn't legally required to give you that money back for the earlier months. They might do it as a courtesy if you’re a long-time customer, but they don't have to. Your statement is the ticking clock on your consumer protections.

Reconciling: It’s Not Just for Accountants

"Reconciliation" sounds like something a guy in a green eyeshade does in a 1950s movie. In reality, it’s just checking your math. Sometimes a restaurant accidentally inputs a $20.00 tip as $200.00. Sometimes a gas station puts a $100 hold on your account that stays there for a week.

When you reconcile your bank statement, you’re comparing your own records—like your receipts or your tracking app—against the bank's official record. If they don't match, you have a problem. It’s also the best way to catch "phantom" fees. Monthly maintenance fees, out-of-network ATM fees, and "paper statement fees" (ironic, right?) eat away at your savings. If you see a $12 "Monthly Maintenance Fee," call the bank. Often, just having a direct deposit or maintaining a minimum balance of $1,500 will get that waived. But they won't tell you; you have to find it on the statement and ask.

Security and the Digital Paper Trail

In 2026, most of us have switched to "e-statements." It saves trees, sure. But it also keeps your financial data out of your physical mailbox, which is a prime target for identity thieves. A stolen bank statement is a goldmine for a fraudster. It has your name, your address, your account type, and a roadmap of your spending habits.

If you still get paper statements, shred them. Don't just throw them in the trash. Use a cross-cut shredder. Identity theft is a nightmare that can take years to untangle, and a discarded statement is often the first "in" for a criminal.

Proving Your Income and "The Big Purchase"

If you’re self-employed, your bank statement is your lifeblood. Freelancers and "gig" workers don't get a neat W-2 at the end of the year. When it's time to rent an apartment or get a mortgage, the underwriter is going to ask for three to six months of statements.

They aren't just looking at the total. They are looking for "NSF" (Non-Sufficient Funds) marks. Even if you have plenty of money now, a single NSF fee from four months ago tells a lender that you might be disorganized or living paycheck to paycheck. It's a red flag. Keeping your statements clean is just as important as having a high credit score.

The "Check" Problem

Believe it or not, people still use paper checks. If you’re one of them, your bank statement will usually include "cancelled checks" or at least images of them. Check these images. Check the endorsements on the back. Check fraud is actually on the rise again because it's become easier for criminals to "wash" checks—using chemicals to erase the payee and amount and writing in their own. If the image on your statement shows a check made out to "Cash" that you know you wrote to "Landlord," you need to freeze your account immediately.

Actionable Steps to Take Right Now

Stop treating your financial records like a "someday" project. You need to be proactive.

Download your last three months of statements. Don't just look at the screen; actually download the PDFs. Banks usually only keep these online for a few years. If you need to prove something from five years ago for an IRS audit, and you didn't save the file, you might have to pay the bank $5 or $10 per page to pull it from their archives.

Highlight every recurring charge. If you see a name you don't recognize, look it up. If you haven't used the service in thirty days, cancel it. This is the fastest "raise" you will ever give yourself.

Check for fee-free alternatives. If your bank statement shows you’re paying $10 or $15 a month just to have the account open, you’re at the wrong bank. There are dozens of online-only banks and local credit unions that offer totally free checking.

Set an "Audit Date." Pick one day a month—maybe the 5th or the 20th, whenever your cycle ends—to spend ten minutes looking at the transactions. Ten minutes once a month can save you thousands of dollars in fraud losses or forgotten subscriptions over a lifetime.

Managing your money isn't about complex stock picks or high-frequency trading. It’s about the basics. It’s about knowing exactly where every cent goes. Your bank statement is the map; you just have to actually look at it.