City traders are not typically prone to panic over a few hundred lost council seats in the English shires. Local elections are usually dismissed as white noise—a chance for voters to vent about bin collections and potholes without touching the levers of national power. But the mood in the Square Mile this week has shifted from cautious observation to active defensive positioning. The 10-year Gilt yield, that sensitive barometer of British fiscal sanity, is twitching.

The primary concern is not just that Keir Starmer might lose; it is who might win the subsequent argument within his own party. As results from the May 2026 local elections trickle in, showing a fractured electorate and a bleeding Labour heartland, the bond market is pricing in the return of the "bond vigilantes." If Starmer is weakened, the carefully curated "iron discipline" of Chancellor Rachel Reeves is the first thing that will be fed into the shredder.

The Ghost of Fiscal Credibility

For the past two years, the Treasury has operated under a self-imposed regime of fiscal restraint designed specifically to soothe the nerves of global debt markets. It was a strategy born from the trauma of 2022, intended to prove that Labour could be trusted with the nation’s credit card. However, that credibility is now viewed as a fragile truce rather than a permanent settlement.

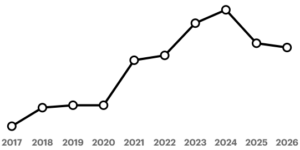

Traders are watching the "swing to the left" not as a mere ideological shift, but as a mathematical inevitability. When a government loses its popular mandate, the traditional response is to spend its way back into the public’s good graces. In the current climate, with Gilt yields already hovering near 5% due to global energy shocks and Middle Eastern instability, there is zero margin for error.

If the local election drubbing forces Starmer to appease his backbenches with promises of "investment" (the polite Westminster term for borrowing), the market will react with cold, hard numbers. We are already seeing the spread between UK Gilts and German Bunds widen. This is a clear signal that international investors are demanding a higher "instability premium" to hold British debt.

The Burnham Shadow and the Leadership Vacuum

The anxiety in the trading pits is focused on specific names. While Starmer remains in Number 10, the "safety" of the status quo is maintained. But the moment his authority is questioned, the market begins to model a Rayner or Burnham premiership.

Andy Burnham, the Mayor of Greater Manchester, has long been viewed by the City as the champion of a more interventionist, high-spending northern agenda. Angela Rayner represents the industrial, union-backed wing of the party that views the current fiscal rules as a straightjacket. To a bond trader, these figures represent a move away from the "Reeves-nomics" of stability and toward a model of unfunded aspirations.

A hypothetical scenario currently being discussed in hedge fund offices involves a "unity" platform that relaxes the debt-to-GDP targets to fund public sector pay rises and green energy infrastructure. While socially popular, such a move would require a massive increase in Gilt issuance. When supply goes up and confidence goes down, prices crash.

Why the Middle East Makes This Worse

No political crisis happens in a vacuum. The current volatility in the Gilt market is being amplified by the ongoing conflict in the Middle East, which has kept inflation expectations stubbornly high. The Bank of England is trapped. It cannot easily cut rates to support a sagging economy if the government is simultaneously pumping money into the system to survive a leadership crisis.

Investors are looking at the UK and seeing a "twin deficit" problem—fiscal and political. If the local elections confirm that Labour is losing its grip on the center ground, the pressure to pivot left will become an existential threat to the party.

The Gilt market is essentially a giant betting machine on the future of the British economy. Right now, the smart money is betting that Starmer’s "iron" rules are about to turn into lead. If the government cannot maintain discipline when the polling gets tough, it won't be able to maintain it when the markets get tough.

The Hidden Cost of Political Survival

The real danger is a slow-motion collapse of confidence. It doesn't require a "mini-budget" style explosion to cause damage. A series of small concessions—a billion here for local government, a billion there for transport—slowly erodes the narrative of stability.

Traders are already moving into "short" positions on sterling and long-dated Gilts. They are preparing for a summer of discontent where the Prime Minister is more worried about his MPs than his creditors. This is the ultimate trap for a Labour government. They spent years convincing the City they had changed, only for a few hundred council seats to potentially undo it all.

The message from the markets is blunt. They don't care about the social necessity of the spending; they care about who is going to pay for it. If the answer is "the future taxpayer" via increased debt, the 5% yield we see today will look like a bargain compared to what is coming. The political "swing to the left" is, in financial terms, a swing toward higher borrowing costs for every homeowner in the country.

The era of cheap debt is over, and the era of political leeway ended with it.